How Connected HVAC Products Can Earn Revenue from the Grid

From $60 per residential AC to hundreds per commercial unit: why grid operators are paying connected HVAC fleets to do less

Published

March 24, 2026

Author

Henrik Holen

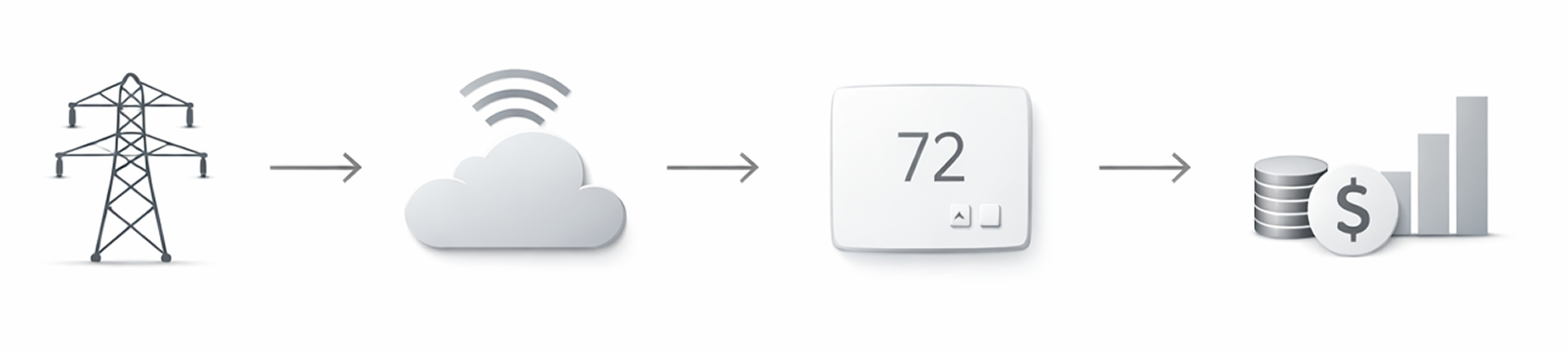

Demand response programs pay connected device fleets to reduce energy load during peak demand. For HVAC OEMs and service providers, this turns IoT connectivity from a cost into a revenue stream.

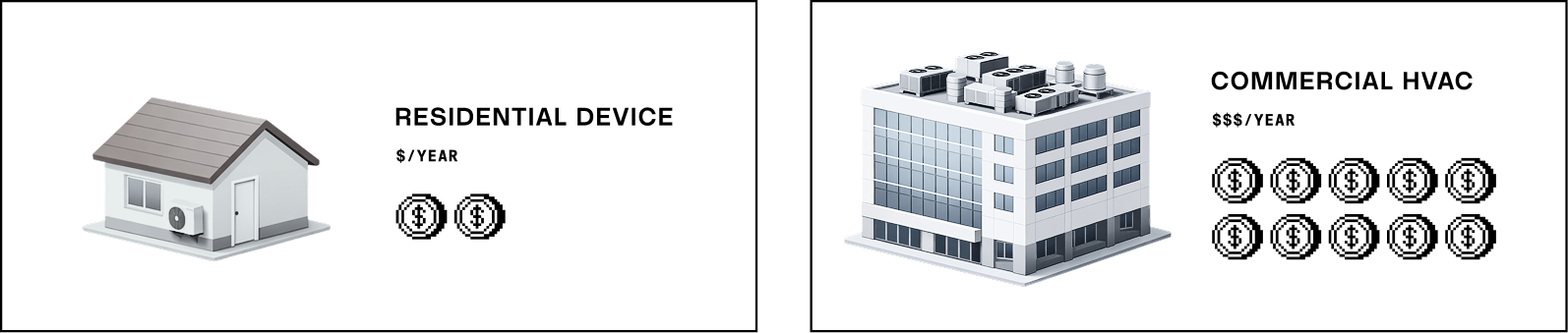

Windmill, a connected window AC manufacturer, rewards its customers with up to $60 per unit per year in incentives through its Eco Rewards demand response program. Google Nest has over a million households enrolled in Rush Hour Rewards, earning $25+ per thermostat each summer. These are small residential devices shedding less than a kilowatt each.

Scale that up to commercial HVAC equipment, where each unit can shed 5-20 kW, and the revenue per device grows proportionally. That is what demand response is. And for HVAC OEMs and service providers managing larger fleets of larger equipment, it turns IoT connectivity from an overhead line into a revenue opportunity.

What Is Demand Response?

When electricity demand spikes, grid operators have two options: fire up expensive peaker plants, or pay connected devices to temporarily reduce their load. The second option is cheaper, cleaner, and increasingly automated.

Demand response isn’t new. Utilities have run programs with large industrial facilities for decades. What’s changed is that fleets of smaller connected devices, smart thermostats, heat pumps, water heaters, commercial HVAC systems, can now participate programmatically through virtual power plant (VPP) platforms.

How much can devices earn? It depends on the size of the load they can shed. Grid operators pay per kilowatt of capacity enrolled, typically $75-150 per kW per year for fast-responding assets. A residential window AC shedding 0.5 kW earns modestly: Windmill’s Eco Rewards pays up to $60/year per unit. Nest’s Rush Hour Rewards pays $25+ per summer across more than a million enrolled households. But a commercial rooftop unit shedding 5-10 kW could earn several hundred dollars per year at those same capacity rates. The bigger the equipment, the bigger the revenue per device.

The traditional business case for connecting products is defensive. You invest in connectivity, cloud, and app development, then hope the monitoring and control features justify the cost. For many OEMs, that’s a hard sell internally.

Demand response flips the equation. Connected products generate revenue. The connectivity investment has a measurable payback period. Instead of “this heat pump has an app,” the sales pitch becomes “this heat pump pays for its own connectivity and then some.”

For service providers managing equipment fleets, DR revenue is recurring, fully automated once set up, and scales linearly with fleet size. Every new device enrolled is additional revenue with no additional operational effort.

For product companies evaluating IoT platforms, that shifts the conversation. Connectivity isn’t just a cost of doing business anymore.

How It Works

Whether you’re connecting products for the first time or migrating an existing fleet, the path to demand response participation follows the same steps.

Connect your devices. Add an ESP32, cellular module, or gateway to your hardware. Build device management and a branded mobile app on an IoT platform that supports remote parameter control, not just monitoring. Read-only telemetry can’t participate in DR. You need the ability to adjust setpoints, modes, and schedules from the cloud.

Check eligibility. Not every region has active DR programs, but coverage is expanding fast. All seven US ISOs have active programs (PJM, CAISO, ERCOT, ISO-NE, NYISO, MISO, SPP), and FERC Order 2222 is opening wholesale markets to aggregated devices through 2026-2027. In Europe, the EU Network Code on Demand Response is expected to create harmonized market access by 2027, with Germany, the UK, and the Nordics leading adoption. The platform checks which deployed devices are in eligible areas based on location data.

Enroll end users. Customers opt in through a simple in-app flow: select their utility provider, authorize participation, done. This takes minutes, not paperwork. The enrollment experience should be built into the app from day one, not retrofitted later.

Respond to grid events. When the grid needs relief, the VPP platform sends a dispatch signal. The IoT platform receives it, targets the right devices, and adjusts parameters automatically. A thermostat setpoint might shift by 2-3 degrees for an hour or two. A water heater might delay its heating cycle. The adjustment is subtle enough that end users barely notice, especially with HVAC equipment where thermal mass means buildings hold their temperature for hours.

Recover automatically. When the event ends, devices revert to their original settings. No manual intervention, no user complaints. This is the critical piece that protects end user experience: participation is invisible unless someone checks the app during an event.

Settle revenue. Participation is tracked, performance is measured, and payments are settled through the grid services program. The VPP platform handles the energy market complexity. Your IoT platform handles the device control.

What Your IoT Software Platform Needs

Enabling demand response requires more from your IoT platform than standard monitoring and control. On top of the basics (fleet management, remote parameter control, white-label mobile apps), DR participation needs:

Regional eligibility management to track which devices qualify based on location

An enrollment flow that lets end users authorize participation through the app

Event dispatch to receive signals from VPP providers, target the right device segments, and apply parameter changes across the fleet

Automatic state restoration so devices revert to original settings when events end

Admin tools for fleet targeting by region or segment, reusable parameter presets, and event monitoring

Most of the energy market complexity, utility relationships, program enrollment, revenue settlement, lives on the VPP partner side. But the device control layer is what makes participation possible. If your platform can’t write parameters to devices in real time, segment fleets by geography, and manage state across events, DR isn’t an option.

Blynk’s platform handles device management, remote control via datastreams, user segmentation, and white-label mobile apps as standard. The demand response layer builds on top: eligibility checking, enrollment flows, event dispatch, and automatic state management.

Windmill, a connected AC manufacturer running on Blynk, already does this. Their Eco Rewards program dispatches events through Leap’s VPP platform on weekday afternoons from May to September. During peak demand, Windmill’s cloud adjusts AC setpoints slightly or switches units to fan mode. Users get notified in advance, can opt out of any event, and most don’t notice any change. Participants earn up to $60/year per AC in rewards. It’s a window AC shedding less than a kilowatt. Scale that to commercial heat pumps or a fleet of rooftop units, each shedding 5-20 kW, and the per-device revenue scales with the load.

The Virtual Power Plant Ecosystem

A fleet of connected HVAC devices is, in energy market terms, a virtual power plant. It’s distributed generation capacity that can be dispatched like a traditional power plant, just by reducing demand instead of producing supply.

VPP platforms handle the market access layer: connecting device fleets to grid services programs, managing dispatch signals, and settling payments. Companies like Leap, Virtual Peaker, Enode, and Enel VPP Connect operate in this space. They need partners with connected device fleets. The IoT platform is the bridge between the physical devices and the energy markets.

Leap alone manages 400,000+ energy sites and devices, has 100+ technology partners, and grew capacity by 100% year-over-year in 2025. Next Kraftwerke aggregates 7.5 GW across 15 European power exchanges. Renew Home (the Google Nest spinout) controls ~3 GW and is targeting 50 GW by 2030.

North America has ~33 GW of enrolled DR capacity today. The DOE wants 80-160 GW by 2030. Utilities are actively recruiting distributed energy resources because paying connected devices to reduce peak load is cheaper than building new power capacity. For OEMs, that means the market is pulling, not pushing. VPP platforms want your devices enrolled.

Europe is 2-3 years behind the US but moving fast. The EU Network Code on Demand Response, proposed in March 2025, will establish harmonized rules for integrating demand-side flexibility into European electricity markets. Germany leads with 28% of the European VPP market. The UK, Nordics, and France are active. The European VPP market alone is projected to grow from $2.6 billion to over $16 billion by 2034. OEMs who build connectivity now will be positioned when the European market matures.

Multiple device types qualify: smart thermostats, heat pumps, AC units, water heaters, battery storage systems, EV chargers. HVAC equipment is the sweet spot because thermal mass means you can shift load without impacting comfort. A building holds its temperature for hours after the HVAC adjusts. That makes HVAC the easiest sell to end users and the most reliable performer for grid operators.

Designing for Demand Response

If you’re planning connected products, factor DR into your architecture from the start:

Pick the right hardware. ESP32-based controllers with WiFi handle most residential and light commercial applications. Cellular modules or LoRaWAN gateways cover distributed commercial deployments where WiFi isn’t available. If your equipment already has a main controller, Blynk.NCP pairs it with an ESP32 as a dedicated network co-processor. Your MCU runs the application logic. The ESP32 handles WiFi, BLE-assisted provisioning, cloud connectivity, and OTA firmware updates for both chips. Your engineering team doesn’t need to rewrite their firmware stack to get connected.

Choose a platform that writes, not just reads. Remote monitoring platforms can’t participate in DR. You need writable datastreams: the ability to adjust setpoints, switch modes, and modify schedules from the cloud. This is also what enables remote support, predictive maintenance, and automated energy optimization, so the investment pays off beyond DR alone.

Build enrollment into your IoT app early. DR participation requires user consent and utility authorization. Design this into the onboarding flow, not as an afterthought. A banner after device setup, a simple utility selection screen, and a clear explanation of what happens during events.

Think regionally. DR programs vary by market. In the US, all seven ISOs have active programs, with PJM (8,500+ MW enrolled), CAISO, and ERCOT being the largest. In Europe, Germany, the UK, and the Nordics lead, with broader EU market access coming through the Network Code on DR by 2027. Your platform should handle eligibility by location so you can expand into new markets without rebuilding.

Run the numbers. Grid capacity payments run $75-150 per enrolled kW per year. A fleet of 10,000 commercial HVAC units each shedding 5 kW is 50 MW of enrolled capacity. Even at the low end of capacity rates, that’s meaningful revenue that didn’t exist before you connected the product. The exact numbers depend on your equipment size, region, and VPP partner, but the exercise is worth doing early.

Blynk’s IoT software platform handles device management, branded mobile apps, remote control, and demand response capability. Whether you’re connecting your first product line or migrating an existing fleet, explore what Blynk can do for HVAC.

Sign up for a newsletter

Get latest news from Blynk

Over 500,000 people already signed up our newsletter. We never spam.

Thank you! Your submission has been received.

Oops! Something went wrong while submitting the form.

.png)